Understanding the Dynamics of Interest Rates and Mortgage Trends

Dear Clients,

I hope this message finds you well.

I wanted to take a moment to shed some light on the recent developments in interest rates and mortgage trends, particularly in light of the actions taken by the Czech National Bank and their impact on the mortgage market.

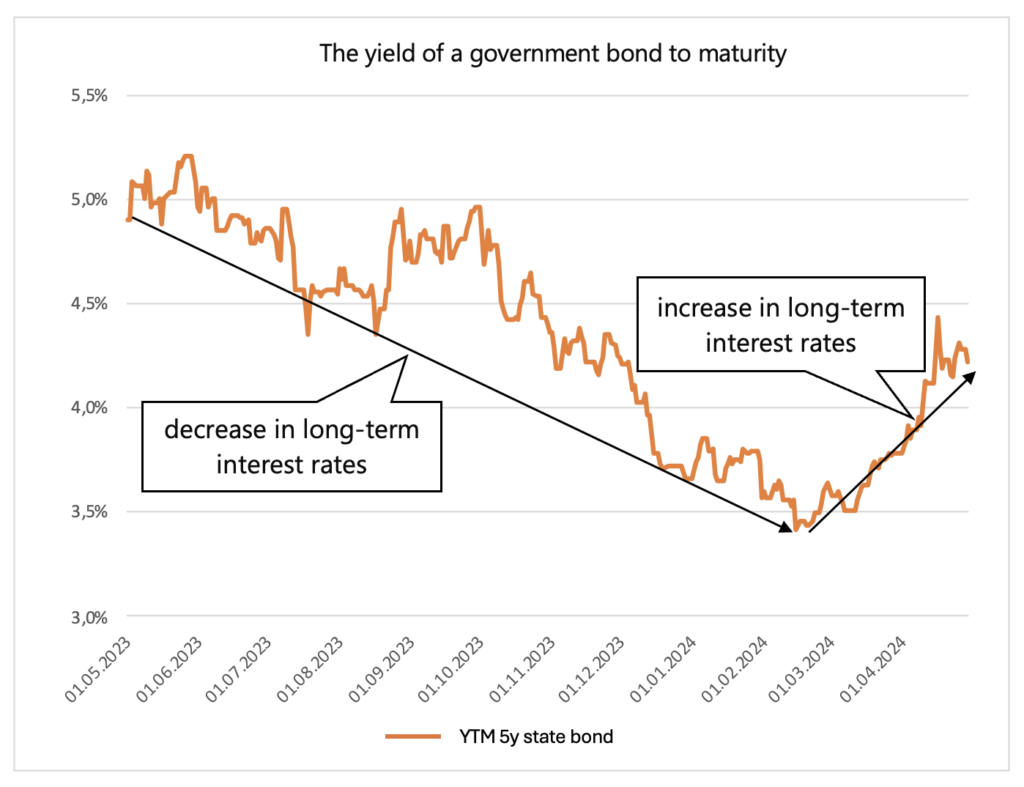

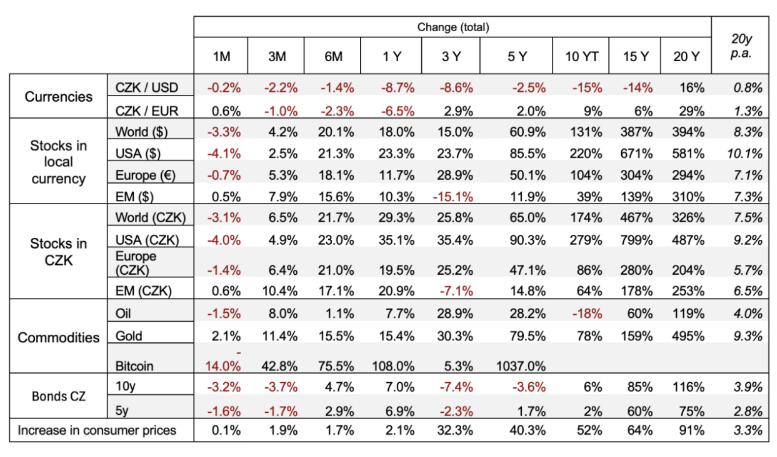

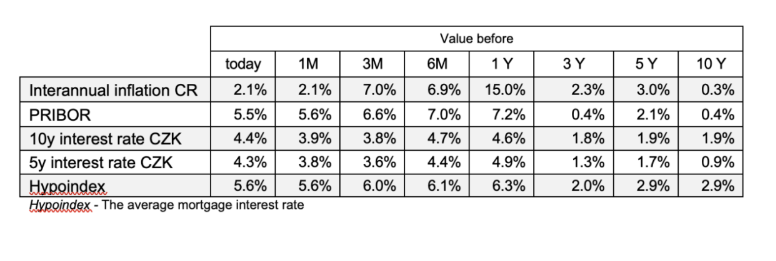

You may have noticed that despite the Czech National Bank lowering interest rates, mortgage rates have not seen a corresponding decrease. It’s crucial to understand that this is not due to any malice on the part of banks, but rather a result of the distinction between short-term and long-term interest rates. The Czech National Bank influences short-term interest rates, but mortgages, such as a 5-year fixed rate, are tied to long-term (e.g., 5-year) interest rates. And short-term rates differ from long-term rates. For example, six months ago, short-term rates were 7%, but mortgages were offered at 6%. And 5-year government bonds yielded only 4.4%. Investors expected inflation to be tamed and the Czech National Bank to reduce interest rates gradually. That’s why they borrowed at 4.4% for 5 years. Over the past year, long-term interest rates have also declined. That’s why mortgage rates have also fallen. A year ago, mortgages (according to the Hypoindex) were at 6.27%, and now they are at 5.57%. However, the decline in mortgage rates has stopped, and some banks have even increased mortgage rates. The reason is the rise in the prices of resources. 5-year interest rates are 0.7 percentage points higher compared to February 2024.

The yields of government bonds also influence the value of bond funds. A rise in yields over the last 3 months means a decline in bond prices. (We’ll talk about that next time). When deciding on a mortgage, don’t speculate on a decrease in interest rates, and don’t rely on the fact that interest rates must fall. The mechanism of rates is more complex and cannot be described by the assumption: Inflation will be tamed – the Czech National Bank will lower rates – and mortgages must be cheaper. It may not happen, or not right away. If you’re considering a new mortgage or your existing mortgage’s fixation period is ending, please feel free to reach out to me. I’m here to assist you in determining the optimal term and duration of the fixed interest rate.

If you’re curious about the behavior of financial markets last month and the underlying reasons, please continue reading.

At its April meeting, the Federal Reserve decided to keep interest rates at their current level. The Fed is waiting for inflation to approach its 2% target more rapidly. The slow fight against inflation is a mild disappointment for financial markets, as more successful inflation management and faster interest rate cuts were expected. In response, global stock markets saw a decline of 3.3% in USD and 3.1% in CZK. However, this decline was not significant, as stock markets simply returned to the level they were at during March.

In the Czech market, inflation is being successfully reduced. Last month, year-on-year inflation was 2%, and prices rose by only 0.1% month-on-month. Therefore, the Czech National Bank lowered interest rates by half a percentage point to 5.25%.

—

V.I.P. Senior Consultant VII

Partners Financial Services, a.s.

Nové sady 2, 6.p.

602 00 Brno