Supplementary Pension Plan (DPS) vs Long-Term Investment Product (DIP)

The DIP (Long-term Investment Product) is discussed everywhere.

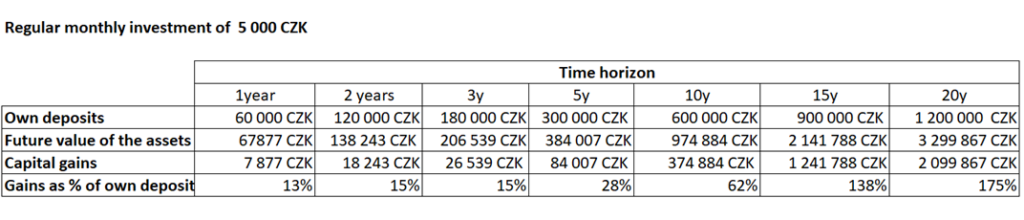

The day will not run away if we do not encounter an article about the long-term Investment Product (DIP) in the media. DIP is based on long-term regular investments. Therefore, let’s remember how regular investment works and see what a regular investment in stock markets would look like in the past.

With a short-term investment (1-3 years), profit from regular investment was uninteresting. It did not help to get rich in any way. Capital gains in investment for 10 years have already been more than half of their deposits. With a regular investment of CZK 5,000 per month, we invested 600 000 CZK in total, and the capital profit was CZK 374,000. Capital gains in investing for 15 or 20 years exceeded their deposits

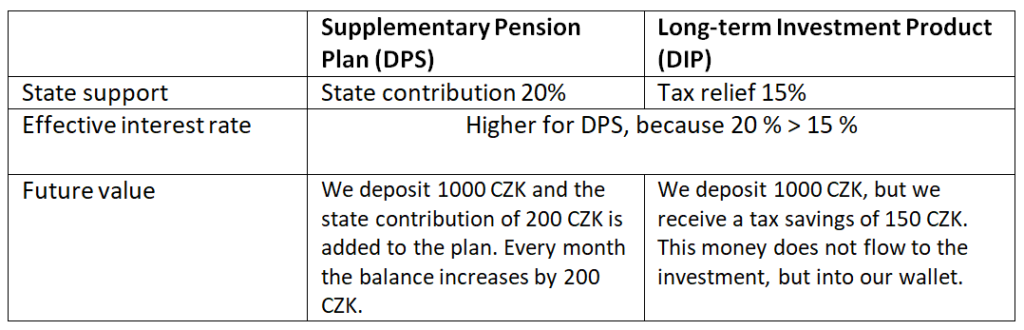

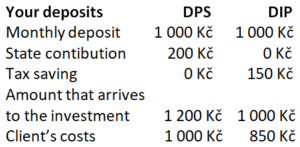

The Supplementary Pension Plan (in Czech, called DPS) is also about regular investments. So what makes DIP “better”? DIP allows you to invest in various financial products that can offer potentially higher appreciation, obtain tax relief, and allow contributions from the employer.

You can’t compare the total amount, but the effective interest! If we use an example of 1000 CZK for 20 years and an expected appreciation of 5%, the effective interest in this case will be higher for DIP.

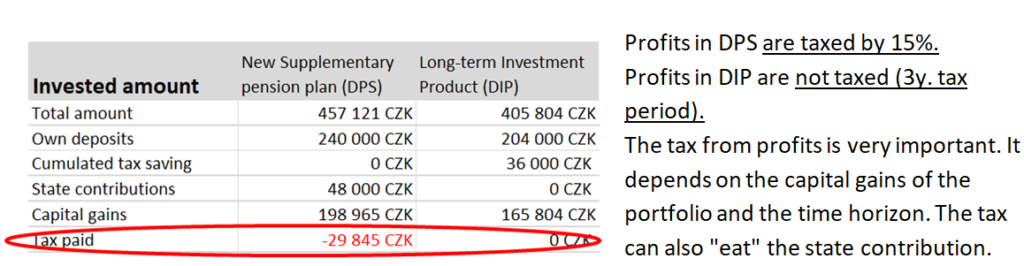

But if we just change the parameters of the investment slightly, the result will be different. The tax deduction helps DIP and is more important for shorter contracts (10 years). For longer horizons, capital gains are crucial; tax savings are insignificant.

Parameters of DIP say that the contract must last at least 10 years and at least until the age of 60. The money deposited in DIP cannot be withdrawn prematurely. You would lose tax benefits and have to pay back the tax. When choosing DIP as a product to build assets for your retirement, the tax savings are not the most important; the properties of regular investment and the selection of a suitable product are. It is necessary to look primarily at the costs and the correctly chosen strategy allocation. It has more power than tax deductions and decides what volume of money you will have in your portfolio at the end! Properly set DIP can significantly help build assets for your retirement and financial independence.

For expats who are not 100% sure if they will stay in the Czech Republic until the age of 60, it is important to carefully consider whether you want to “lock” your investment in DIP. Instead of DIP, you can use the same investment (without a state contribution in the form of a tax deduction and employer’s contribution) and have money available at any time, with premature withdrawals possible. I highly recommend that you consult your situation with a financial specialist who understands DIP and its pros and cons and will help you set the portfolio for your retirement optimally.

V.I.P. Senior Consultant VII

Partners Financial Services, a.s.

Nové sady 2, 6.p.

602 00 Brno